“Rich people use debt to leverage investments and grow cash flows. Poor people use debt to buy things that make rich people richer.” — Grant Cardone (Businessman)

No prices for guessing in which category most of us fall. There’s another bad habit that the average person has regarding debt: Not leveraging the already owned assets for better offerings.

The payment is due tomorrow, so you need that money in your hands right now instead of waiting days for banks to clear the loan. Also, putting your assets as collateral makes your interest rates considerably lower.

This makes a lot of difference in emergencies, which most likely strike when you’re least prepared. That medical bill or that home repair suddenly comes, and you don’t have enough savings to pay for it.

In this article, I’ll answer why leveraging assets against debt is smart. The following sections will list the best borrowing options when you own something of value, and avoid any mistakes while doing that, so your finances stay secure.

KEY TAKEAWAYS

- Money emergencies mostly strike when you’re low on cash.

- Loans take a very long for getting approved and charge pretty high interest rates.

- Putting your assets as collateral against borrowing cash is a great strategy.

- This allows for fast cash at lower interest rates.

First, some stats. As per a survey, 59% of Americans can’t cover a $1,000 emergency expense with their savings. That means the majority of this country cannot handle a financial emergency.

What’s more, Bankrate’s recent report showed that 1 in 4 Americans have NO emergency savings. Zippo. Nada. Zero dollars saved for an unexpected situation.

That leaves millions of Americans in need of quick cash.

And that’s exactly where asset-based borrowing options come into play. Rather than jumping through hoops with banks and credit unions, you can leverage something you own to secure what you need… quickly.

Let’s back up for a second.

When you leverage what you own, you’re using assets like vehicles, property, or valuables to your advantage. These assets can be used as collateral for a loan – allowing you to access fast cash without the long wait associated with conventional loans.

Borrowing options vary based on interest rates, approval times, and the associated risk. But if you own something of value, the following ones are the best way forward to get fast and cheap cash.

Need emergency cash FAST?

Consider a vehicle title credit.

Car title pawn options make it possible to quickly access title pawn fast cash when time is not on your side. But how does it work?

A vehicle title loan allows borrowers to use their car title as collateral for a short-term credit. You hand over the title, receive your loan amount and continue driving like normal while paying the money back.

Pros?

If speed is your main concern, vehicle title loans are the way to go. They remove many of the obstacles that prevent traditional lenders from giving you title pawn cash ASAP.

Keep in mind. Always ensure you can make your repayments before signing any contracts. Borrow responsibly.

Homeowners have the option to take out what’s called a HELOC, or home equity line of credit.

Simply explained, it allows you to borrow against the built up equity in your home. Because these loans are backed by your property, they typically come with lower interest rates than other options. Beyond HELOCs, there are various other ways to get a debt consolidation loan depending on your financial goals. And if you fail to make payments your home is at risk.

This type of asset-based credit works best for borrowers who have time to wait for funds, and need larger sums of money.

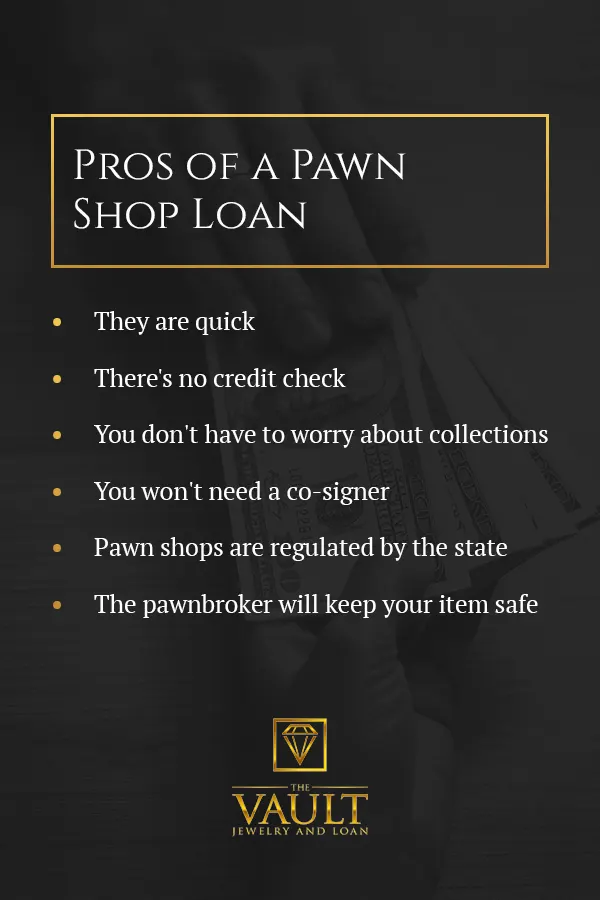

Pawnshops allow you to borrow small amounts of money against personal items.

Example? Jewelry. Electronics. Collectibles.

You hand over an item to the pawnshop. In return, they give you a loan based on the item’s value. The huge perk is that you typically receive those funds right away. The following infographic lists all the benefits of a pawn shop credit:

Alt: Pawn Shop Loan Benefits

The downside? Pawn shops usually lend small amounts. And if you fail to pay back the loan, your item is sold.

These loans are best suited for small, short-term emergencies.

Borrowing money against assets is a smart strategy, but not completely safe; nothing is.

Consider this…

Smart vs. reckless borrowing is determined before you even sign the credit agreement. If you follow these tips, you’re already on your way to borrowing responsibly when you own something of value.

Simple tips. But following them can mean the difference between using debt as a tool… and having debt rule your life.

Hint: if you’re unsure of how you’ll be able to pay the money back within the agreed timeframe, explore other options first.

When everything is fine, most of us are confident about our money management. But when we’re low on cash and emergencies arise, the brain doesn’t work properly, we tend to make bad decisions, and even forget many things.

Here are a few mistakes you’ll want to avoid when borrowing against something you own.

Interest rates, hidden fees, rollover charges. You name it.

If you fail to read the terms of your loan agreement, you’re asking for trouble. Borrowers often get excited about getting money that they overlook key conditions. Don’t become “that” borrower.

Stick to one lender. When you take out loans with multiple lenders, you’re putting yourself at risk for falling into a debt cycle. Since these loans are short term, it’s easy to see how you might not be able to repay your initial loan – causing you to take out additional loans.

All lenders are different. Just because you qualify for credit with Bob’s Loan House doesn’t mean you should accept their terms without shopping around.

Ask around. Check online reviews. Then compare at least 2-3 options before submitting any paperwork.

Just because you can… doesn’t always mean you should.

Using your home or car as collateral is risky. Without a rock-solid repayment plan in place, you shouldn’t use these as collateral. If you fail to pay back the loan, you put your chance of having a place to live OR transportation at risk.

When you need emergency money, the best way is to simply put your asset at stake as collateral. It eliminates the wait of traditional bank loans and opens your options when every second counts.

To review…

If done responsibly, lending against your assets can be your best friend when an emergency hits. Just remember to follow the tips above and borrow smart.

Ans: Capacity, Capital, Collateral, and Character.

Ans: Invest the debt in income-generating or appreciating assets.

Ans: Various assets like financial securities, real estate, jewelry, FDs, and even insurance policies.

Ans: Of course, you can use them as collateral.