With an advancement in technology and rapid growth, fraud during onboarding and fake customer profiles haveturned into a latest trend.

This can adversely impact the workculture of industries, organisations, and institutions specialty those dealing with financial matters such as financial institutions.

Especially when the job requirements of such institutions require people across diverse fields, ranging from traditional to non-traditional applicants.

So, if you wish to find out how to carry out smooth onboarding for your institution, read on further to know!

Key Takeaways

- Understanding the needs of non-traditional applicants in financial institutions

- Carrying out identification and verifying the applicants before selection

- Analysing the risks involved in bringing different applicants on board

- Providing the onboarding training to ensure compliance with regulations by the new hires.

- Bringing up a balance in risk and ensuring the financial inclusion of all

- Going through the diligence procedure to have a fair review

The first line of defence in onboarding is identity verification.

It is very important to verify an employee before bringing them onboard to avoid any future consequences.

Modern institutions use advanced digital verification tools that combine document scanning, biometric recognition, and database cross-checks.

The rising trends of multi-factor authentication adds another layer of security.

Instead of relying on a password alone, applicants move ahead with the idea of biometric confirmation, secure authentication to have avail a secure environment.

Background checks are yet another important step. Even when applicants have limited records, institutions assess consistency across the data they can access.

The goal is not to exclude. It is to verify with confidence.

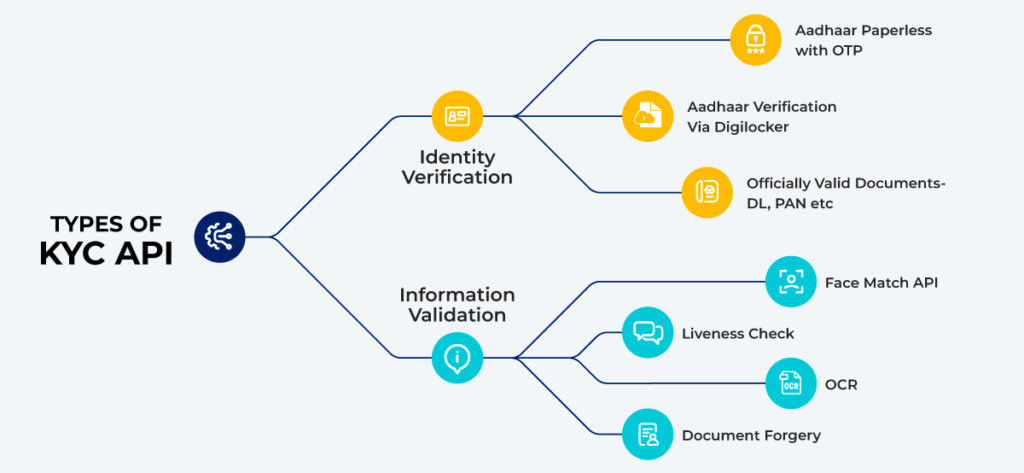

The identification and verification of candidates can further be observed in the infographic :

After identity verification, institutions move into structured risk evaluation.

It is where data analytics comes into play. Financial institutions analyse the risks involved by studying income patterns, digital footprint, and transaction behaviour to have a clearer picture.

These institutions cater to individuals based on their profiles. For example, an international student has a completely different review structure compared to an entrepreneur, which are considered a highly risky profile.

Such demarcations make onboarding controls easily accessible and contribute to better compliance with the risk decisions.

This collaboration reduces legal exposure while maintaining operational efficiency.

For higher-risk profiles, enhanced due diligence procedures provide a deeper review.

This involves a line of interviews to access :

Another key advancement is utilising the transaction monitoring systems.

It helps in tracking unusual activity patterns in real time.

This includes accounts held by first-time applicants with no prior banking history, as well as a bank account for international students managing funds across borders.

Regular audits of onboarding workflows ensure that due diligence remains consistent and aligned with internal policies.

Risk management does not operate in isolation. Regulatory compliance forms the foundation.

Adherence to the regulations is very important for the smooth functioning of institutions involved in money matters, such as financial institutions.

When the customer trust is built into the institution, it becomes important to follow the protocols to have a good reputation.

Technology, again, plays a key rolein ensuring this regulation. It helps in :

Automated reporting systems further reduce manual error and improve response time.

The ongoing training, therefore, ensures that staff understand regulatory updates and procedural adjustments.

When we refer to balancing risk in financial inclusion, we don’t refer to limiting the opportunities or cutting down the access. We rather mean taking risks that are balanced and ensure financial inclusion as well.

A common trait amongst the non- traditional applications is that they contribute to economic growth, stepping out of the rigid legacy models. Their role in digital expansion is yet another important area to consider.

If look up to the future and contemporary developing policies, it can be witnessed that the onboarding process is likely to turn towards AI for actions such as resume selections, interviews, smooth onboarding, etc.

With the evolution of the financial institutions, the ones that focus on the inclusivity of diverse applicants, followed by enhanced security, are likely to benefit more.

Ans: When we talk about risk management, risks can be classified into four categories: strategic risk, operational risk, financial risk, and compliance risk.

Ans: It is important to have face-to-face conversations in order to build long term relationship with customers because people tend to connect more with brands with whom they can speak personally.

Ans: Poor onboarding can negatively impact employee productivity and performance. An unclear definition of roles can confuse and impact the employee’s performance adversely.

Ans: The four key onboarding controls are: compliance, clarification, control, and connection. This ensures a smooth and engaging transition for employees.