“Financial advisors often suggest that post-retirement living expenses willbe about 70% to 80% of pre-retirement expenses.”

To support these initiatives, there are two means by which a person can invest: first, retirement plans, and second, annuities.

Today, in this article, we are going to take a closer look at both of them and give you the best suggestions to make your future planning even better.

Let’s unfold!

Understanding Retirement Plans

A retirement plan is one drawn-up plan that is built with the help of funding and investing for your years in retirement.

These budgeting programs come in various forms and also include working plans such as 401(k) and individual retirement accounts.

In these subscriptions, the donations are typically allowed to grow and are availed of the promise of not paying taxes provided that the particular scheme is adhered to.

The noteworthy distinction with retirement plans is that it’s substantially less stiff compared to an annuity in that you can decide where your money is being put in terms of investments, say into stocks, bonds, and other mutual funds.

One major benefit of retirement plans is their potential for growth over time, especially if you have started saving early. The compounding of such dividends and capital gains made this portfolio increase quite substantially when taken to retirement.

Annuities: A New Twist to Retirement Security

Annuities, in that context, are, therefore, financial products that attempt to give one some sort of flow of income usually for life, and get normally paid from some kind of future date.

Since their investment grows with the time passed, annuities differ from retirement plans since one gives out an insurance company some amount and gets the money in parts of the respective payments made on different periods- immediately or delayed until a future date, according to its type.

Annuities come in many forms: fixed, variable, or indexed. All of these have varying pros and cons. Fixed annuities give you the certainty that you will have a certain rate of return, thus offering stability and predictability to retirees who prefer sure returns.

Variable annuities, however, offer an opportunity for you to invest in various securities and may give more returns; they do come with greater risks.

Although annuity agreements are marketed as a way to guarantee income during retirement, they may not be right for everyone.

For illustration, annuities usually carry high fees and surrender charges if you are forced to take your money before the deadline.

Did you know? The average retirement age in the U.S. is 62, with a life expectancy of approximately 77.5 years, indicating an average retirement span of about 15.5 years. (Investopedia)

Use of Calculators in Finding the Right Option

Given that we now have understood the fundamentals of retirement plans and annuities, the question then is: After all, how do you make your choice? One of the most effective weapons that you can have in your ideal process arsenal is a financial calculator.

By employing these devices, you can analyze the different positives of both the two products which are estimated returns, risk, income streams, and other elements that will decide whether you will be better off with either one.

Retirement Plan Calculators: These tools will inform you of what should be done in the interest of achieving a goodhearted retirement. This calculator is based on your current savings, the money you earn, the age at which you plan to retire, the rate that you would like to make, and inflation.

Then you will be able to figure out just how much you have to save monthly to retire comfortably after incorporating those variables. The most advanced retirement plan calculators take into account income tax slab changes and allow you to estimate the possible tax rates your withdrawals might be taxed at retirement.

A good retirement plan calculator will help you to see the possibilities of these tax implications so that you can make better decisions. Another important feature of these calculators is the ability to simulate different scenarios.

These tools provide a concise, graphical image of the way your money may compound over time so that you can set feasible expectations over your retirement years.

Annuity Calculators: In the same way, annuity calculators make it possible for a person to find out how much money they can have as a regular income by annuity purchase.

One simply types money that they plan to invest the diversity of annuity they want to purchase and the age they would like to retire at, then, the terms of payment for which one wishes to have the annuity listings.

Through this, the system should estimate the monthly payments, taking into consideration interest rates and the type of annuity contract.

One can use annuity calculators to weigh the pros and cons between different types of annuities.

For example, a fixed annuity is more likely to offer fixed payments but at low returns, whereas a variable annuity will have higher returns but is more uncertain.

Comparing the various identities of both will enable you to make the right choice on how you want to allocate your retirement savings.

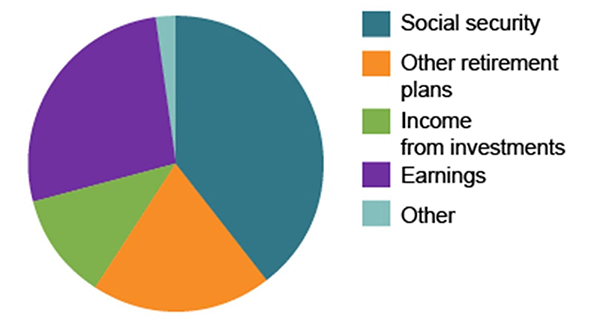

Intriguing Insights This pie chart here shows the demographic of capital generation from different sources of good retirement financial plans.

How to Use Calculators to Improve Retirement Decisions

The best way in which lifetime savings plans and annuity calculators can be optimized is through strategic thinking. First and most significant, one needs to set clear financial goals.

Once your goals are set, you can gather all the retirement plans and annuity calculators at hand to analyze various scenarios.

In many cases, you can ascertain what might impact your plan after some time, like inflation, interest rates, or tax rates.

Ultimately, calculators can enable you to see things more clearly and avoid common mistakes such as underestimating what you will need to save or choosing an annuity with unfavorable terms.

Combining these data-driven insights with your personal financial goals makes you far better able to make informed decisions for your retirement.

Conclusion

In pursuit of a secure retirement, both supplemental retirement plans and annuities have their strengths and weaknesses. Retirement plans can be quite flexible and even offer enormous growth potential.

Annuities, however, will provide predictable income for the rest of your life. Calculators help you weigh these options and forecast what you actually require.

In this manner, you can design a retirement strategy that guarantees financial security and peace of consciousness, all based on your carefully evaluated goals, risk tolerance, and projected future expenses.