Loans are a vital part of the life of many Americans. They need loans to be able to buy the necessary things for everyday life – things such as homes or vehicles.

Loans can also be used to pay for costly repairs. Almost everyone has a loan out for something.

Other things that to use loans for are weddings, family trips, and remodeling homes. For some of these things, one might want to save because, for example, people would not want to start their married life in debt. Some people need loans just to get through everyday life.

Many lenders would love to assist people to get a loan. We suggest trying forbrukslån.no/kredittlån to see what they have to offer. They usually have many different lenders that would be able to help someone in need.

This article will help readers to learn more about loans and how they can get them. It will also let them know what needs to be done before getting one. Despite this, we advise doing more research to find the information required.

1. What Can You Afford? Decide what you can afford to pay each month for the loan payments. Secure funds to repay it and get a picture of how much one can pay.

Don’t forget to remember that the payments can last for years. In case of inability to afford anything extra each month, it’s better off not getting one.

The amount of money that one can afford each month will decide how much to borrow. Also, consider interest rates and other fees when planning to get one.

These payments need to be figured into what one can afford. However, the inability to afford all the fees means inability to afford the loan.

2. How Will You Use the Money? See how you are going to use the borrowed money. As was mentioned above, there are many ways to use the money.

Although, one does not want to use it for something frivolous. But, when using the money for something frivolous, they are less likely to pay it off in full and will ruin the credit report.

Think about what you need the money for – something such as a home or vehicle, for instance.

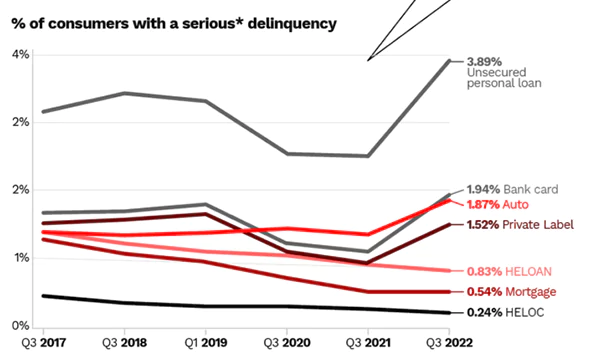

Statistics:The graph mentioned above demonstrates key consumer credit delinquency levels rising from Q3 2017 to Q3 2022.

People also get money for consolidating other debts so that they have only one payment each month instead of many.

Even, the money can be utilized to finally have that vacation that you have dreamed about for years.

Being a supreme authority, you get to decide what to do with the money most of the time.

3. Secured and Unsecured Loans – Loans can be secured or unsecured, depending on why someone is borrowing the money.

Secured means that people will need to have some sort of collateral to borrow the money.

Collateral could be anything of value that would cover the loan. If there is a default on the loan, the lender will take the collateral.

On the other hand, unsecured loans do not require any collateral. They depend on the credit history and credit scores.

Do You Know?: In the second quarter of 2023, the unsecured personal loan debt reached a record $232 billion with the average outstanding balance amounting to an all-time high of $11,548.

The better the history and scores, the better interest rates will people get. Luckily, there are ways to improve these things.

4. Do not Apply for Too Many at Once – It Is advised to avoid applying for too many loans at once. Since every application will show up on the credit report.

The more applications that show up, the more damage it can do. So, take it easy on applying and avoid damaging the report.

Perform thorough research before applying – check out all the details of the loan. Compare interest rates and other fees.

Some of the other fees that one might have to pay are origination fees and prepayment penalties. These could all add up to extra money for the cost of the loan.

5. Bigger Loans Equal Less Interest – Be sure to check the interest rates of the loans for which you will apply. One way to save on interest rates is to borrow more money.

This can be applied while not having problems paying back the money. Want to save interest? This is one way that allows people to do that.

Another way to save on interest fees is to make sure that the recognition report is clean and there are no red flags on it. If the report has red flags, remove them by reporting any mistakes and paying off old debts.

Doing this will assist in having a great report and a high credit score. This will make it easier to get loans whenever needed.

6. Personal Credit – As was mentioned above, personal credit is the most integral thing that requires special attention. Having a poor report will make the process tougher to get a loan.

There are ways to take care of this, consider applying them. If these are not taken care of, you will likely be denied the loan.

Lenders can even check their personal recognition history when applying for a business loan. This will just show the bank how well one pays back their debts.

In the case of a bad history of paying back debts, there are fewer chances of getting a loan. Make sure to keep the credit history clean to borrow money when needed.

7. Business Credit – Applying for a business loan? Make sure that the business credit score is good, too. You can check out this article to learn how to check the business credit score.

This is more difficult to check than your personal credit history. It can be done, but requires a small amount for it to happen. This might seem like an investment.

There are businesses where people can check things such as outstanding liens, judgments, and other things. They can also fix these problems just as they could with their credit report.

Fix these things before applying for a loan. Check with the agencies that take care of business loans so that you can fix any problems.

8. Watch Bank Statements –Keep an eye on bank statements because the lenders will be. These are almost as decisive as the credit history.

The lender will look at these to see how well one pays their bills. Buying frivolous items and not paying bills, lessens the chances to get a loan.

With outstanding loans, make sure that you are paying debts on time. This will help you when you are applying for new ones.

Therefore, having a good history can be a game changer.

9. You Might Not Get Advertised Rates – Many factors come into play before people can get the advertised interest rates.

The lender will look at the credit report, bank statements, work history, and many other things before they determine what the rates should be. Even if everything is perfect, other factors could come into play.

Lenders are required to give these rates to at least fifty-one percent of their customers. This means that the best of the best will get these rates.

In case of something fishy in history, you probably will not get the best rates. So, it’s decisive to have a perfect history of paying the bills on time, as well as having a great work history.

10. Loans are the Means to an End –Don’t take out a loan just for the sake of taking one out. One should have a good reason to get one – such as debt consolidation or buying a home or automobile.

If you are someone at risk of declining your home or auto, get a personal loan to catch up on the payments. These are good reasons to borrow money.

Interesting Fact: Back in Ancient Egypt, if the borrower failed to repay the loan he went to prison or became a slave to the lender.

Understand that, loans are a means to an end and not the end to a means. This means that you want to make sure that you do not rely too much on loans.

These are a few details that one needs to know to get a loan. Just make sure that you need the money and that you are not getting it for something frivolous.

Do not use loans to pay off gambling debts because this will only get you into more trouble.

Keep working hard to have a clean credit report and a good credit score before applying. If needed, there are ways to fix a bad report and raise that score.

A business report can be fixed if you have the means to do so.

Also Read: Why Installment Loans are a Smart Financial Choice