Getting a loan is a moment when no delays can be managed. Whether you want to increase your business, buy new equipment, or improve your cash flow, in any of these situations, delays and disapproval can ruin your expectations.

Imagine you have found the right lender, discussed the deal, and are done with formalities. Then you found out that one missing document has extended your verification process. Business loans don’t just rely on your credit score; they are heavily driven by the required paperwork. Missing it can shake your financial stability and business credibility.

Read this article to know how missing documents can result in the delay of your business loan approval. And learn how not to get stuck during the business loan application process.

Key Takeaways

- Incomplete documents can put a break on your application, and may result in the disapproval of the loan.

- Identity proof, financial records, and documents like ITR are required for a loan approval.

- Missing any of the incomplete documents may result in delays and an extended verification process.

- Many of the loan applications are rejected due to the unavailability of updated documents.

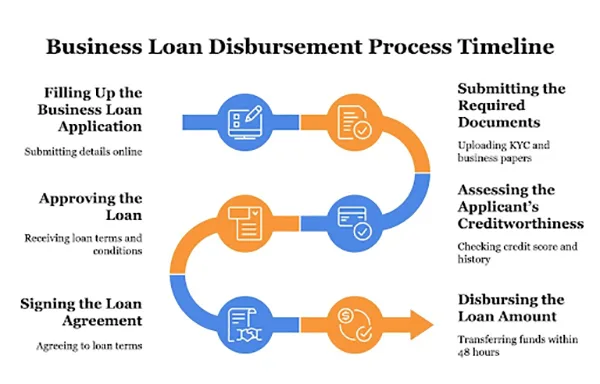

In a business loan application, documents allow lenders to check the authenticity of the business, repayment capacity, and how compliant the business is with regulations. The application is incomplete if the required documents are missing. This requires the lender to re-verify details and increase the time taken to provide approval. In some cases, it may lead to rejection of the loan application.

While the exact list of documents required varies among lenders, there are a few mandatory documents. Some of them are as follows.

Missing documents can have the following impact on your business loan application.

Delays caused by missing documents can ruin your expectations and may result in business instability. Explore the steps mentioned below to avoid delays due to missing documents.

Surprising Fact

In the financial year 2024-2025, over 8.18 crore ITRs were filed, and half of them were first-time taxpayers.

Most of the borrowers are unaware of the common documents required, which results in delays. Those common documents are:

While some lenders may allow borrowers extra time to submit the necessary or correct documents, the application might be considered incomplete or non-compliant. This may result in the rejection of the application.

The time taken to receive approval for your business loan depends on how complete and accurate your documents are. Even small mismatches in the information provided may extend the approval timelines or lead to rejection. To avoid delays, businesses can prepare a checklist of the necessary documents, update their records, and make digital copies of the necessary documents. Proper documents can increase the chances of business loan approval.

Ans: By providing the required documents on time, delays can be avoided. Homeowners generally miss the common documents, which causes delays.

Ans: Common documents that borrowers miss are updated Aadhaar proof and recent bank statements.

Ans: ITR(Income Tax Documents) is a file that has your personal information, such as your annual income and the deducted tax on your salary, and more.

Ans: Documents like an Aadhaar card and a PAN card can be used as proof of identity.